There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

{{DATE}}

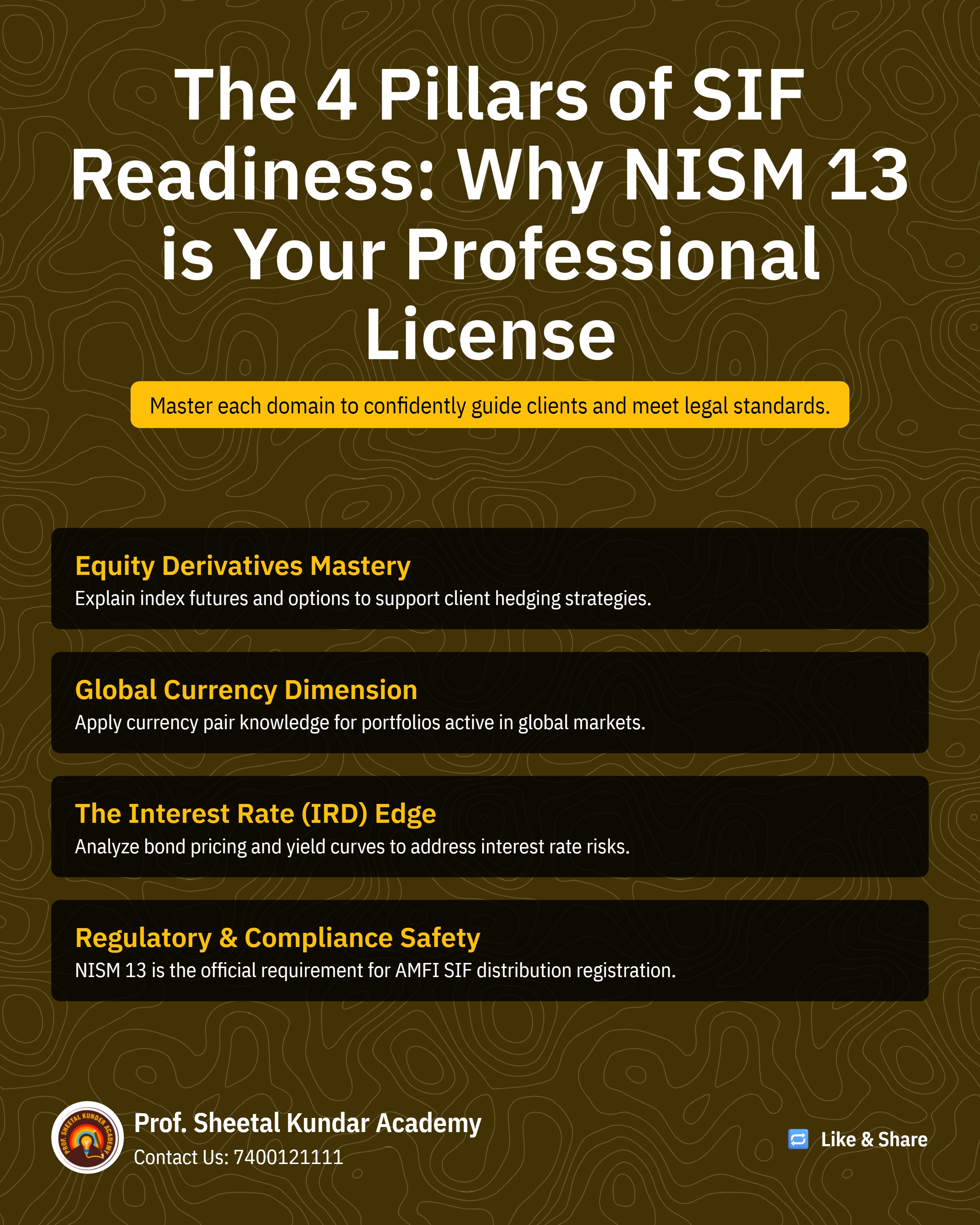

SEBI's introduction of Specialised Investment Funds has changed the rules for every Mutual Fund Distributor in India. SIFs are not just a new product category. They represent a structural shift in how affluent investors will allocate money going forward, and SEBI has made the NISM Series XIII Common Derivatives certification mandatory for every distributor who wants to participate.If you are an MFD or finance professional who has not yet cleared NISM Series XIII, you are already locked out of one of the fastest-growing product categories in the Indian financial market. This post explains why SIFs matter, what SEBI's mandate means for your practice, and why clearing NISM Series XIII is the single most important professional step you can take right now.

What Is a SIF and Why It Finally Makes Sense for Serious Indian Investors

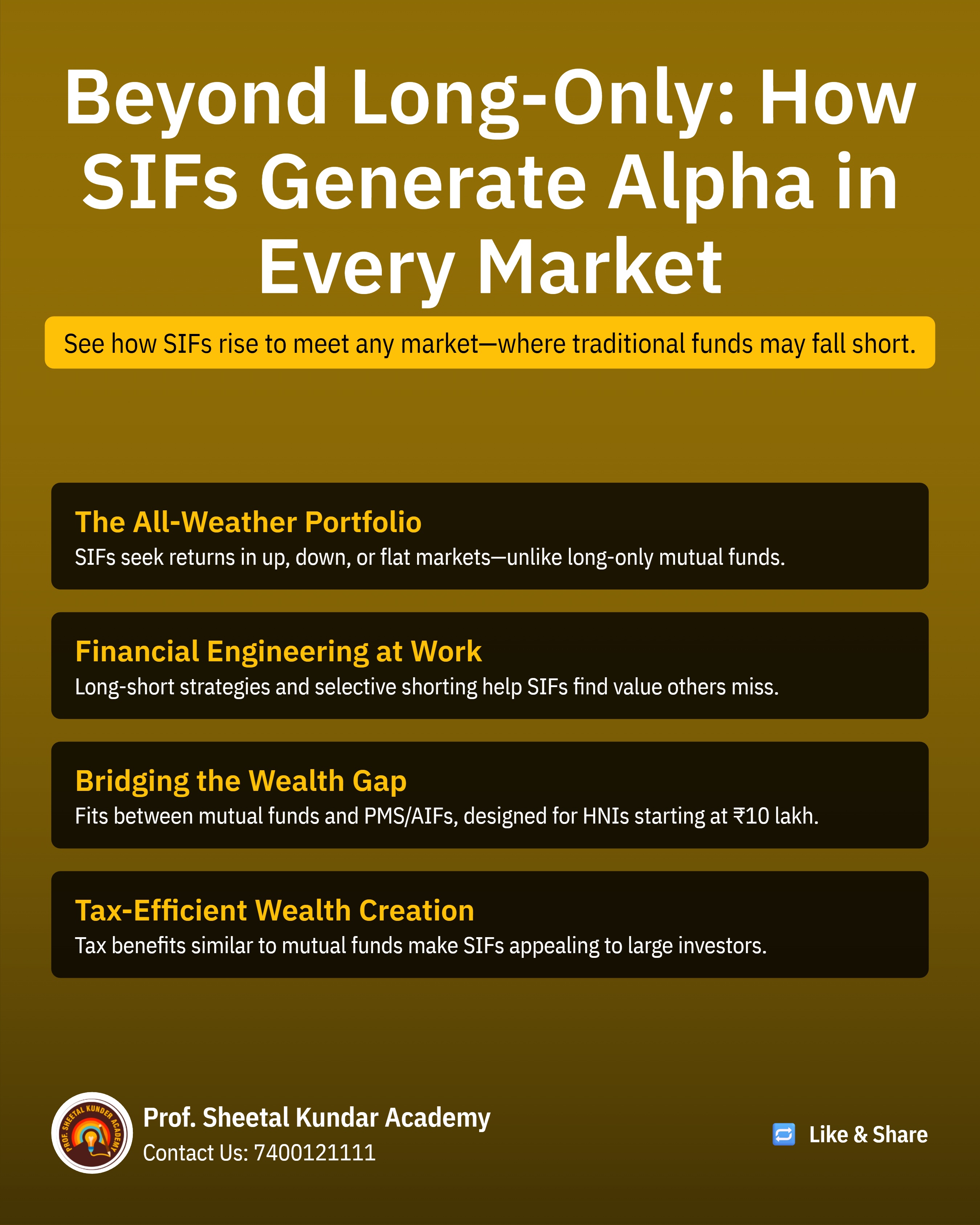

India's investment landscape has long had a gap that no one has properly addressed. Traditional mutual funds are accessible but rigid. They can only buy stocks, follow strict allocation rules, and have no room for complex positioning. Portfolio Management Services offer flexibility but demand a minimum of ₹50 lakh to enter. For the large and growing segment of serious, financially informed investors sitting between these two, there was no right product.SEBI addressed this with Specialised Investment Funds. The minimum is ₹10 lakh per AMC, and fund managers gain strategic flexibility previously available only to ultra-high-net-worth investors. The framework became live on April 1, 2025.The core difference from a regular mutual fund is the ability to go short. A traditional equity fund can only buy stocks and wait for prices to rise. A SIF manager can take short positions through derivatives, up to 25% of the fund's net assets, enabling the fund to generate returns when markets fall. This changes the product's nature entirely. It is no longer purely a bet on market direction.SIFs can be equity-oriented, debt-oriented, or hybrid, and within each category, there are further strategy types including long-short equity, sector rotation, and debt long-short. The bar for launching one is also deliberately high. An AMC needs either three years of track record with over ₹10,000 crore in AUM, or a CIO with a decade of experience managing at least ₹5,000 crore. This filter keeps opportunistic launches out and ensures only institutions with real capability enter the space.For an investor who has outgrown SIPs but is not ready for the PMS minimum, SIFs are the first genuinely new option India has produced in a long time. And for every MFD who wants to serve that investor, NISM Series XIII is the only way in.

What Makes SIFs Different From Regular Mutual Funds

| Parameter | Details |

| Full Name | NISM-Series-XIII: Common Derivatives Certification Examination |

| Also Known As | NISM XIII, NISM Series XIII, SIF Exam, SIF Examination NISM |

| Total Questions | 150 |

| Maximum Marks | 150 (1 mark per question) |

| Duration | 180 minutes (3 hours) |

| Passing Score | 60% - 90 out of 150 |

| Negative Marking | 25% per wrong answer |

| Certificate Validity | 3 years |

| Mode | Online, computer-based at NISM test centres |

| Exam Fee | Rs. 3,000+ (payment gateway charges extra) |

Derivatives are financial engineering. They cannot be explained by simple buy-low, sell-high logic. Individual option buyers consistently struggle to generate returns because derivatives require expertise, capital, and disciplined risk management that most retail participants lack.SIFs solve this by delegating derivatives execution to expert fund managers. The client gets access to sophisticated strategies. The MFD's role is to bridge the gap between that complexity and the client's understanding.To do that effectively, you need to know:

{{AUTHOR}}

SIFs use derivatives as their core operating instruments. SEBI mandated NISM Series XIII to ensure every distributor handling SIF products has verified conceptual knowledge of equity, currency, and interest rate derivatives before advising or selling to clients.

SIFs are regulated under the mutual fund framework with a minimum ticket size of Rs. 10 lakh. PMS typically requires Rs. 50 lakh minimum, and AIFs require Rs. 1 crore minimum. SIFs offer more sophisticated derivative-based strategies than regular mutual funds but with lower entry barriers than PMS or AIFs.

Yes. SIF fund managers can take unhedged short derivative positions of up to 25% of the portfolio. This allows the fund to generate alpha in bearish and sideways market conditions, unlike long-only mutual funds, which depend on a rising market.

ICICI Prudential, SBI Mutual Fund, Mirae Asset, Nippon India, and HDFC Mutual Fund have launched SIF products. The category collected thousands of crores in AUM within the first few months after launch.

Rs. 3,000 plus payment gateway charges, as listed on the official NISM website.

An MFD with NISM Series XIII certification can explain why a SIF fund is positioned a certain way, how it generates returns in different market conditions, and why it is more suitable than individual options trading for an HNI client. This depth of knowledge directly builds client trust and retention.

No. The exam tests conceptual understanding, not trading execution. With structured module-wise preparation, MFDs from mutual fund distribution backgrounds clear it on the first attempt.

30 to 50 days with 1.5 to 2 hours of daily focused study is sufficient. PSKA students have cleared it in as few as 11 days with structured preparation.

Every month without certification is a month where certified competitors can distribute SIF products to your HNI clients. Once those client relationships are established elsewhere, they are difficult to recover.

Yes. PSKA offers 15-day and 60-day flexible plans with extension options at a discount, 25+ calibrated mock tests, and one-on-one doubt-clearing with Prof. Sheetal over video or audio call - structured around a working professional's schedule.

Launch your Graphy

Launch your Graphy