There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

{{DATE}}

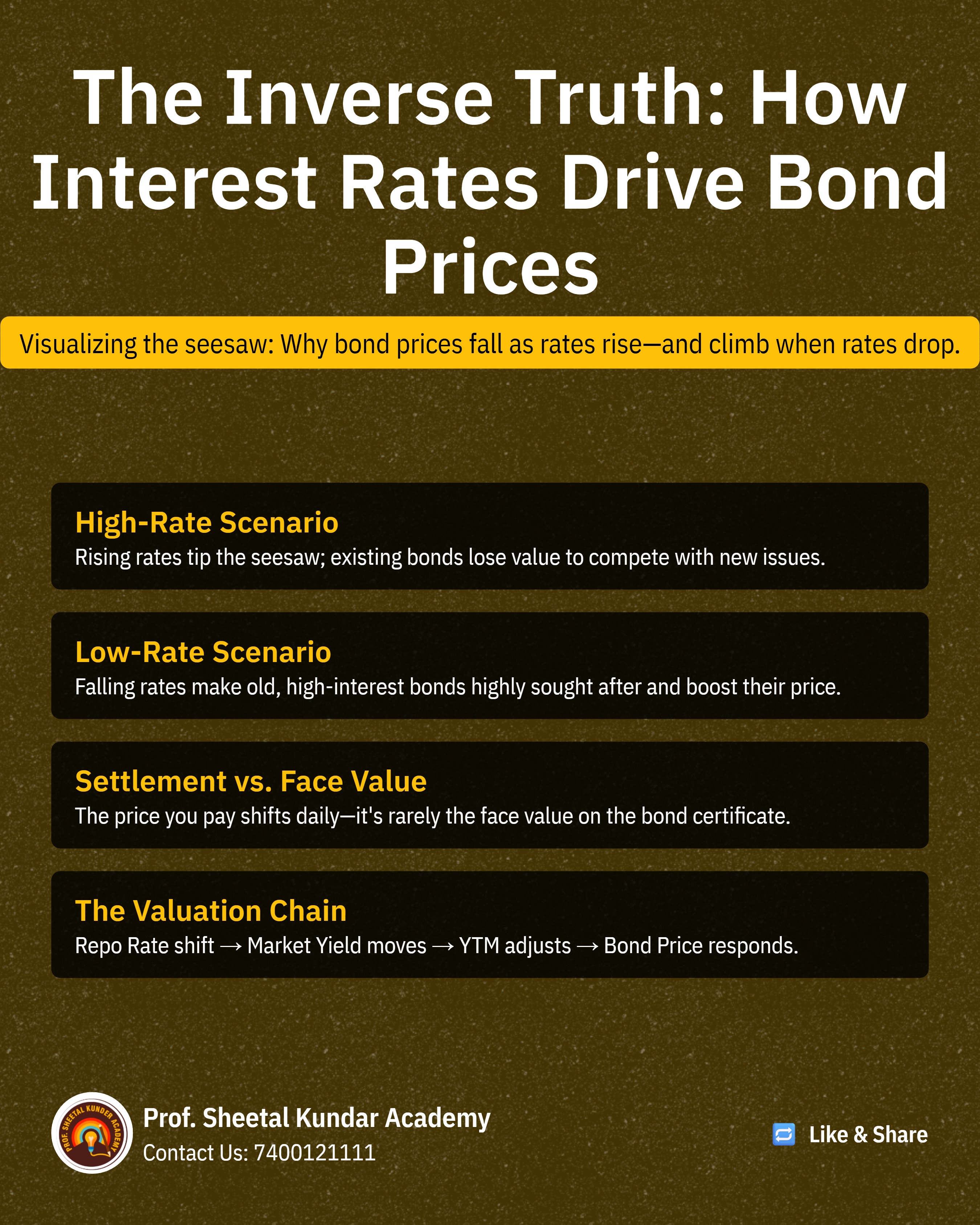

A bond's value fluctuates with prevailing market interest rates. The core relationship, which must be understood by every aspirant, is the inverse relationship between the bond’s yield (or Yield to Maturity, YTM) and its market price.

Rising Interest Rates: When the general interest rate (Repo Rate, etc.) rises in the market, the bond yield increases. To compete with newer, higher-yielding issues, the market price (or value) of the previously issued bond decreases.

Falling Interest Rates: Conversely, if the RBI reduces the Repo Rate, the market yield decreases. The previously issued bond becomes more attractive, and its market price increases.

The market price that the buyer pays the seller is often called the Settlement Value, and it rarely equals the bond's Face Value.

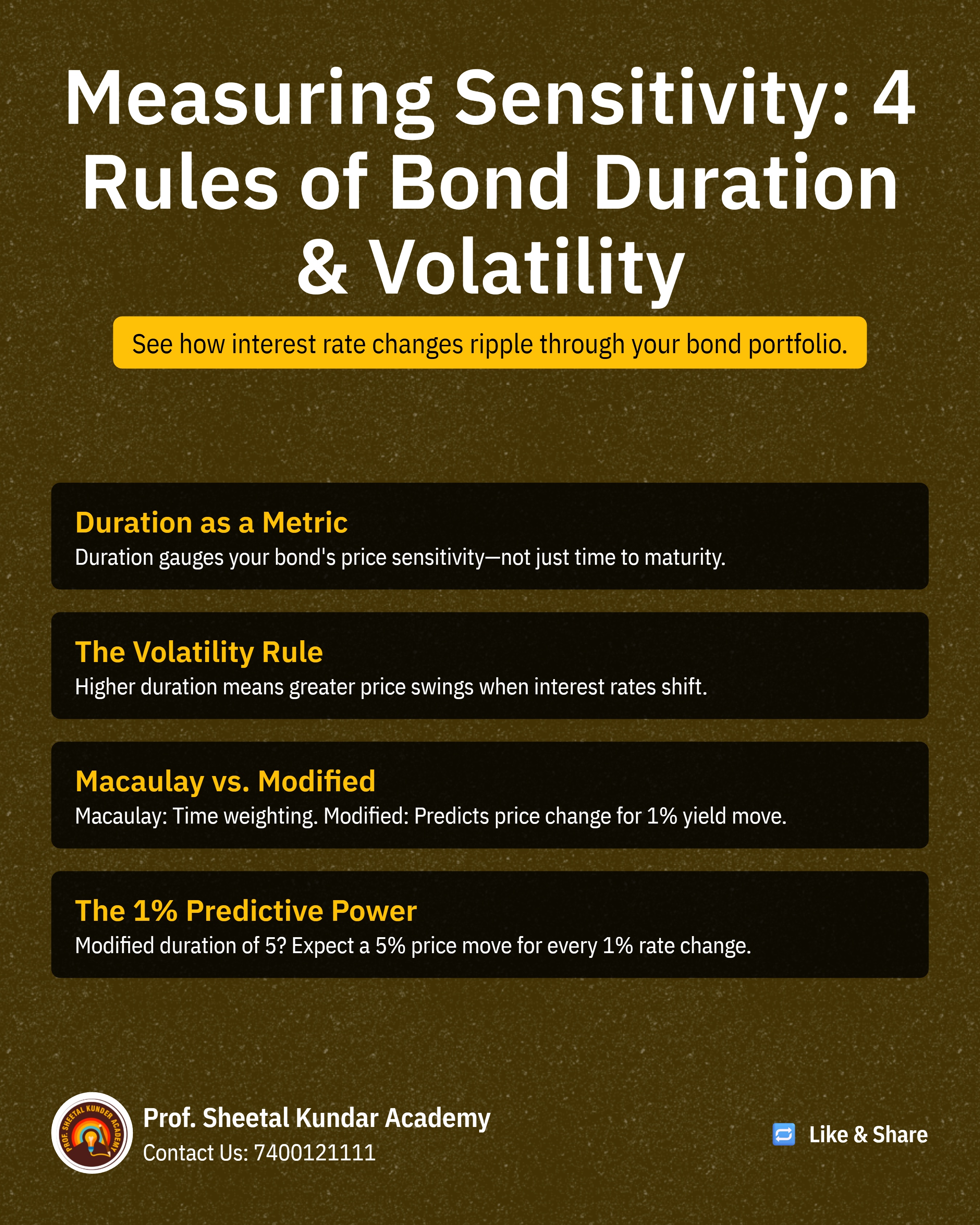

While the inverse relationship is clear, the magnitude of the price change is not uniform. If the bond yield changes by 1%, the price will not necessarily change by exactly 1%. The extent of this fluctuation depends on a critical metric: Duration.

Understanding Duration: Duration tells investors how sensitive a bond's price is to a change in the interest rate or yield. It essentially measures the "risk" associated with interest rate movements.

The Volatility Rule: This leads to a fundamental rule in bond theory: Higher Duration means Higher Price Volatility. This means a long-term bond (which generally has a higher duration) is more vulnerable to interest rate changes than a short-term bond. If you forget this rule in the exam, you can use the calculation methods (which we will cover in subsequent sections) to verify the relationship using simple numbers.

In manual calculations (which are covered in NISM courses), two types of duration are typically computed:

1. Macaulay Duration: This measures the weighted average time until all cash flows (coupons and principal) are received.

2. Modified Duration: This is the practical metric derived from Macaulay Duration that directly measures the percentage change in bond price for a 1% change in the yield.

Modified Duration is the figure that allows for the prediction of price movement. The change in bond value due to a 1% yield change can be estimated using the Modified Duration figure.

It is critical to distinguish between the General Interest Rate (like the Repo Rate) and the Yield to Maturity (YTM).

General Rates Influence YTM: General rates (Repo Rate, RBI rate) are not used directly in the bond valuation formula. Instead, they influence the market's YTM.

YTM is the Valuation Driver: YTM (the yield a bond earns if held to maturity) is the specific rate used to compute the bond value.

The Chain Reaction: RBI raises rates -> Market yield rises -> YTM rises -> Bond Price falls. Conversely, RBI reduces rates -> Market yield falls -> YTM falls -> Bond Price rises.

This understanding of the change in YTM due to general interest rate changes is necessary before proceeding to the actual computation of Duration. This comprehensive theoretical foundation ensures aspirants are fully prepared for the numerical sections of the NISM exams.

{{AUTHOR}}

SEBI® Research Analyst. Registration No. INH000013800 M.Com, M.Phil, B.Ed, PGDFM, Teaching Diploma (in Accounting & Finance) from Cambridge International Examination, UK. Various NISM Certification Holders. Ex-BSE Institute Faculty. 18 years of extensive experience in Accounting & Finance. Faculty Development Programs and Management Development Programs at the PAN India level to create awareness about the emerging trends in the Indian Capital Market and counsel hundreds of students in career choices in the finance area

Launch your Graphy

Launch your Graphy